In the last couple weeks the campaign against the Trans Mountain Pipeline Expansion (TMX) project has been turned up to 11. My social media feed is full of claims like: “100+ economists sent a letter to @JustinTrudeau confirming that #TMX pipeline is massive boondoggle putting billions of tax $$ at risk.” Needless to say, the letter was not signed by “100+ economists” unless you define “economists” to consist primarily of individuals with no credentials or practical experience in the academic field of Economics. Rather, it was signed by a handful of economists and a lot of anti-TMX activists.

One of the major arguments by the “economists” in their letter (and other activists like Tzeporah Berman) is that there will be no demand for Alberta’s oil in a post-pandemic world. More specifically, the letter argues “decline in world oil markets and the escalating construction costs have undermined the viability of TMX and put taxpayers’ money at risk“.

As I will explain in this blog post, the Canadian oil sands industry (producing heavy oil at low cost from facilities with low depletion rates) makes the TMX a good investment in a world with plateauing and/or decreasing oil demand.

Oil Field Decline and Depletion

To understand why oil sands are a good bet you must first understand the concept of oil field decline and depletion. Put in the simplest terms: oil fields don’t last forever. Each oil field has a finite supply of accessible crude and from the day they start pumping every field has a limited lifespan. Some oil fields (particularly the big Saudi fields) have huge supplies that have lasted for decades and will be there for decades to come. But those fields are the exception, not the rule. As Terry Etam explains:

Natural decline rates on petroleum wells/fields is a minimum of about 3 percent and, for new technology like shale fields, something more than twenty percent. Let’s be fairly conservative and say that global decline rates are 7 percent.

On a 100 million b/d base, that would mean that the world would need to add 7 million b/d of production after just one year to keep production flat. Over two years, the petroleum industry needs to add 13.5 million b/d to keep production flat at 100 million b/d.

Yes, you read that right, a shale well can lose 20% of its production in one year. In order to maintain production, at existing rates, new wells have to be drilled pretty much constantly and through the Covid period that has not been happening.

Meanwhile, on the international front, the majors and super-majors have significantly cut back on their exploration and development budgets and have put major projects on hold. What does this mean to oil sands producers?

Well contrary to the activist claims, it is good news for the Alberta oil sands. Unlike their competitors, oils sands projects have very low depletion rates with very low break-even points. As IHS Markit puts it:

Even in a low price scenario that sees upstream investment fall sharply, production from Canada’s oil sands does not. Output remains stable and companies would chip away at costs over time, experiencing more production gains by upgrading existing facilities. This scenario is a reminder about the unique nature of Canada’s oil sands. “The absence of meaningful [production] declines makes a future without oil sands growth difficult to see.” [emphasis mine]

As noted in that report, much of the existing oil sands production is profitable at prices over $25/barrel while CNRL recently reported their mining and upgrading operating costs declined to a record low of $17.74 barrel. In a world where the drop in supply is expected to exceed the drop in demand, existing oil sands projects, with their low depletion rates and low break-even costs, will be ideally situated to meet the world’s future oil needs, especially since the oil sands produce heavy crude.

On the Particular Value of Heavy Crude

You might ask why I emphasize the importance of “heavy crude” since the activists like to claim that heavy crude is inferior to light crude. That is a common misconception.

Heavy oil is neither better nor worse than light crude. They are distinct products that have similar, but not the same, markets. Heavy crude needs to be refined in specially designed and built high-conversion refineries. These high-conversion refineries include expensive cracking and coking units, designed to break down the longer and heavier hydrocarbons into the smaller units used in gasoline, kerosene and diesel.

The simpler light crude refineries, meanwhile, don’t typically have these cracking and coking units. Ironically, this can mean that the light crude refineries can’t handle the heavier components in the light crude oils and so these refineries end up producing more undesirable byproducts (like petroleum coke) per barrel of input.

What this means is that the heavy oil refineries produce more gasoline/diesel/kerosene per barrel of heavy crude oil than the light refineries do per barrel of light crude oil. As a bonus the complex heavy refineries produce a lot less waste petroleum coke per barrel which also reduces their costs.

This difference is called the “coking margin“. For the last couple decades the coking margin has exceeded the “crack spread” [the difference between the input costs and output value in a typical refinery]. As described in this document for the 10-year period between 1995 to 2005 the USGC Maya coking margin averaged $3.63 per barrel above the average of crack spread of $3.46 per barrel. That number has only increased in the intervening decades. That is why so many refinery owners have invested to increase the complexity of their refineries.

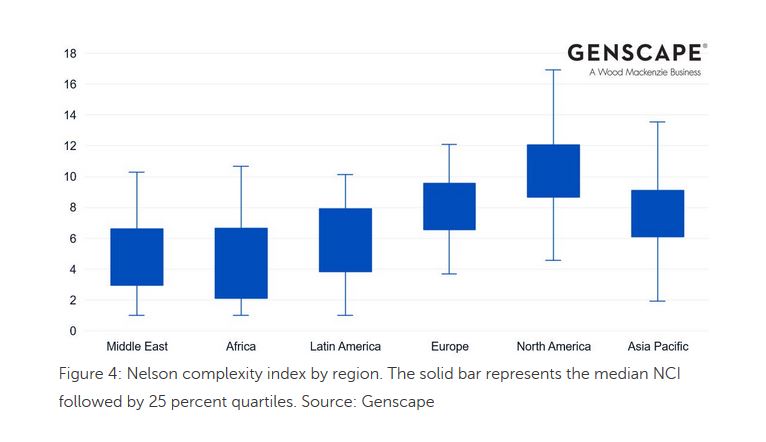

To explain the jargon, the Nelson Complexity Index is a measure of the sophistication of an oil refinery, where more complex refineries are able to produce more heavily refined, and valuable, products from a barrel of oil.

Having invested heavily into building these complex refineries, the owners will pay to get the heavy oil that optimizes their returns. This is why the light-heavy price differential has mostly disappeared in the last couple years.

As for the supply side of the equation, for decades Venezuela was a major exporter of heavy oil but thanks to bad government and lack of investment Venezuela has dropped from exporting close to 3 million barrels a day in 2000 to nearly zero in 2020. That 3 million barrels a day is almost 6 times the volume that can be moved in Line 2 of the TMX. Now let’s look at what has happened on the demand side for heavy crude.

Asian Refining Capacity

One of the most bizarre recent narratives presented by the activist community is that there is no market for diluted bitumen in Asia and that Asian refineries can’t refine dilbit. This is entirely untrue.

Historically the American Gulf coast refineries have been the pinnacle of refining complexity. This is no longer the case. As presented in this document these days Asian refineries are approaching the complexity of the US fleet.

Many of the region’s refineries are new and are optimized to process heavy and sour crudes.

So, contrary to what the activists have to say Asia has a lot of refineries that can refine heavy oil. Want some numbers? According to GlobalData:

The global refinery fluid catalytic cracking units (FCCU) capacity increased from 19,926 mbd [thousand barrels a day] in 2014 to 21,050 mbd in 2019 at an AAGR of 1.1 percent. It is expected to increase from 21,050 mbd in 2019 to 22,240 mbd in 2024 at an AAGR of 1.1 percent. United States, China, India, Japan and Russia are the top five countries in the world accounting for 61.2 percent of total FCCU capacity in 2019.

Asia’s FCCU capacity is expected to increase by 542 mbdfrom 8,385 mbd in 2020 to about 8,927 mbd in 2024. Out of the Asia’s total capacity additions, 151.2 mbd is likely to come from the expansion of active projects while the remaining 391 mbd is expected to come from new-build planned projects.

Finally as described in another report:

GlobalData’s report,‘Global Refinery Coking Units Outlook to 2024 – Capacity and Capital Expenditure Outlook with Details of All Operating and Planned Coking Units’, reveals that Asia’s coking capacity is expected to increase by 374 mbd, from 3,489 mbd in 2020 to about 3,863 mbd by 2024

Look at those numbers. Asian refineries can refine over 8 times what Line 2 of the TMX can supply to Westridge Marine Terminal for export.

Conclusion

Let’s summarize the case for the TMX: currently the crude oil market is expected to plateau and then drop. However that drop is not expected to be as steep as the ongoing drop in supply associated with global oil field decline and depletion. Historically, this decline and depletion of existing oil fields has been counteracted by increased investment in exploration and development in the upstream sector. Except most of the majors and super-majors have significantly decreased their investment in exploration and development of new oil fields. The result will be a global decrease in access to new oil fields and in particular to heavy oil. Meanwhile, global refinery owners have spent billions of dollars upgrading their facilities…facilities optimized to refine that increasingly hard to get heavy oil.

Into this world of demand outstripping supply for heavy oil comes the TMX. The TMX will allow Alberta to ship highly desired heavy oil from oil sands facilities that have very low depletion rates, with very low break-even points, to motivated buyers with custom-made facilities designed specifically to refine those heavy crudes. This represents an ideal scenario for Canadian producers. They will have motivated buyers seeking a steady supply of highly-prized oil located where transportation costs to Asia will be minimized, all during a period when global demand for heavy crude is expected to increase. Even in a decreasing market, the strong demand for heavy oil will keep Canadian oil at the top of the order sheet. So much for that letter by those “economists”.

Please unsubscribe me

David G Malcolm

LikeLike

Ty for clarity of the issues…. How refreshingSent from my Samsung Galaxy smartphone.

LikeLike

I have forwarded this post to many of my friends. Their response has been universally positive. Your work is fantastic. Keep it up ! Barry Sullivan

Sent from my iPad

>

LikeLike

good day thanks no one ever tells the truth anymore

LikeLike

Very enlightening.. Thank you.

LikeLike

What we need is a rail system to transport un-diluted bitumen to the west coast. Cheaper and safer than transporting all that diluent, and the tankers could carry 40% more volume per trip.

LikeLike

Oil buy rail raises expenses of transportation. The eagle spirit energy corridor is a great option for getting more product to international markets. Canada should take a serious look into partially upgrading some of our heavy crude as well since it is much cheaper than full upgrading and fetches a higher price on the world markets and no dilution required in the pipeline so you gain 30%+ in capacity. Also finding uses for our oil beyond combustion is great since carbon fiber and composite materials are starting to really take off in many industries.

LikeLike

No…that’s simply uneconomical and impractical…We need the Eagle Spirit project in addition to the TMX expansion.

LikeLike

Pingback: Another day, another flawed CCPA report, this time about the Trans Mountain Expansion Project | A Chemist in Langley

Pingback: Evaluating what the new Canadian Energy Regulator report actually says about the viability of the Trans Mountain Pipeline | A Chemist in Langley

Pingback: Why Climate leaders sometimes build pipelines – understanding the climate implications of the Trans Mountain Pipeline Expansion Project | A Chemist in Langley

Pingback: Understanding the Role of, and Opportunities for, Canadian Fossil Fuels in Our Net Zero Future - A Chemist in Langley - Energy News for the Canadian Oil & Gas Industry - Money Market Advisor